Click on image to enlarge.

Photovoltaics are still, on average, a pricey, subsidy-dependent source of electricity. However, rooftop panels are beginning to beat the grid in a number of jurisdictions with high retail power rates—and their ranks are projected to swell over this decade. A growing number of economists say that rapidly shrinking costs have turned distributed solar generation into a disruptive technology that’s set for runaway growth. In fact, they say, it could ultimately upend the power distribution market.

“We’re completely unprepared for the opportunity that’s going to present itself,” says John Farrell, an economist and senior researcher at the Institute for Local Self-Reliance, a Minneapolis-based economic think tank.

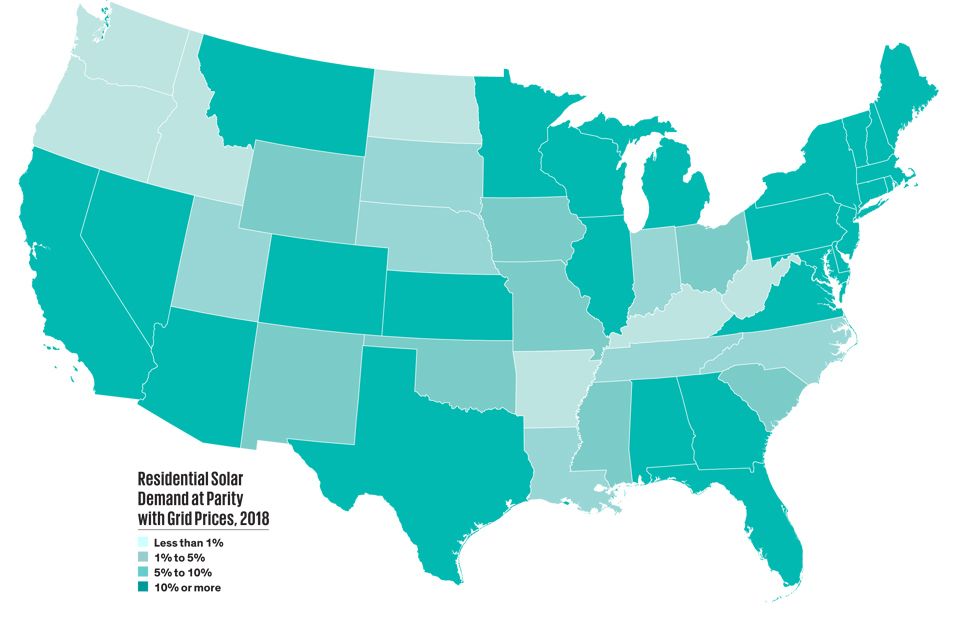

Farrell got beyond the less-inspiring U.S. national average price of rooftop solar on homes and businesses by examining how it stacks up in each of 3100 electric utility rate zones across the country. He projected the per-kilowatt costs of generation from PV systems through 2022 by estimating the cost of installing and maintaining them over their 25-year lifetime and calculating the number of kilowatt-hours they are likely to generate under each zone’s prevailing sunlight. Dividing cost by generation gave him what economists call the levelized cost of solar energy, which he compared to the local utility’s retail power rates.

The results, presented since January as an online map, suggest that rooftop PV already delivers power more cheaply than the U.S. grid for more than 10 percent of residential demand in five states—California, Connecticut, Hawaii, New Hampshire, and New Jersey. By 2022, home panels are predicted to be the economic winner for at least 10 percent of residential demand in 49 states; the grid holds its edge only in the state of Washington, thanks to notoriously gray skies and cheap local hydropower. PV installed by businesses, meanwhile, will be competitive with at least 10 percent of total U.S. commercial power consumption in 2022.

Similar patterns for the United States emerge from academic reviews of PV power cost, such as one published this month by Stanford University researchers in the journal Energy Policy. And a global analysis by the Abu Dhabi–based International Renewable Energy Agency [PDF] last year suggests that PV is at parity in Cyprus and parts of Italy and likely advancing fast.

As with all economic projections, these studies rely on assumptions that are open to criticism. Farrell’s assumptions, however, are relatively conservative. For instance, Farrell does not provide for any change in grid prices, which generally rise by about 2 percent per year. He also excludes federal and state subsidies for solar power installation. Add in the federal incentives and Farrell’s 2022 nationwide parity moment for solar panels arrives in 2018, even in much of dreary Washington state.

The most controversial element in the new economic forecasts for solar is what drives its spread across Farrell’s map as the years pass: the assumption that PV costs will continue to fall. Critics of solar energy attribute its plummeting prices to massive overproduction in China and to subsidy trimming in Europe. According to this argument, prices will rise as more producers go bankrupt (as Solyndra did famously in 2011 and others have since) and supply shrinks.

Stefan Reichelstein, faculty research director at Stanford’s Steyer-Taylor Center for Energy Policy and Finance, however, says the evidence indicates otherwise. His study, in Energy Policy, evaluated the impact of the unusually large price drops in recent years—40 percent in 2011 alone. Replacing PV’s recent dips with an extension of its historic price curve, which has been remarkably smooth for three decades, only increases the levelized cost of today’s systems by 12 to 15 percent. This suggests that the real drivers of PV’s price decline are technology and industrial efficiency, and there is no reason to believe they will hit a wall.

For their part, utilities are providing a strong signal that they recognize the distributed PV price trend, and the threat it represents to their business model: An increasing number of them are petitioning regulators for rate increases targeted specifically at solar users.