This is part of IEEE Spectrum’s special report on the battle for the future of the social Web.

First thing you do, tear this article out of the magazine and carefully set it on fire. It’s about the jockeying for position and revenue among the big players in social media: Facebook, Twitter, and Google’s YouTube. And the analysis isn’t bad for—whaddyacallit—history. But it wasn’t written in the past 12 minutes. So more likely than not it’s already hilariously out of date. (“Google?” you may be asking, perplexed. In case the brand has in the interim disappeared from the scene, like Webvan and John Tesh, listen up: “Google” was a search engine.)

Probably there’s a new serial-killer app in town—CatRattle.com, or some such—that lets users know what everybody else really thinks of them, in real time. Probably sweeping the nation is the phrase “Dude, you’ve been totally rattled.” But just in case events haven’t made a mockery out of this exercise, let’s try to address three basic questions:

1. If you build it and they come, does that guarantee that there’s money to be made? (Hint: No.)

2. Which of Facebook, YouTube, and Twitter will amass the millennium’s first megafortune and a borderless virtual state, with a vast population, political influence, economic clout, and a lair in a hollowed-out volcano from which to control the world’s weather? (Well, you can probably eliminate Twitter.)

3. The Wall Street valuations of companies like Facebook, which is worth US $85 billion on the secondary market, are stratospheric. Should we stockpile ammo and canned goods for when the bubble bursts? (Not a bad idea; remember Pets.com.)

Once again, addressing such questions is a process both complicated and highly speculative. But let’s give it a shot anyway, beginning with a glance at the status quo, and a little arithmetic.

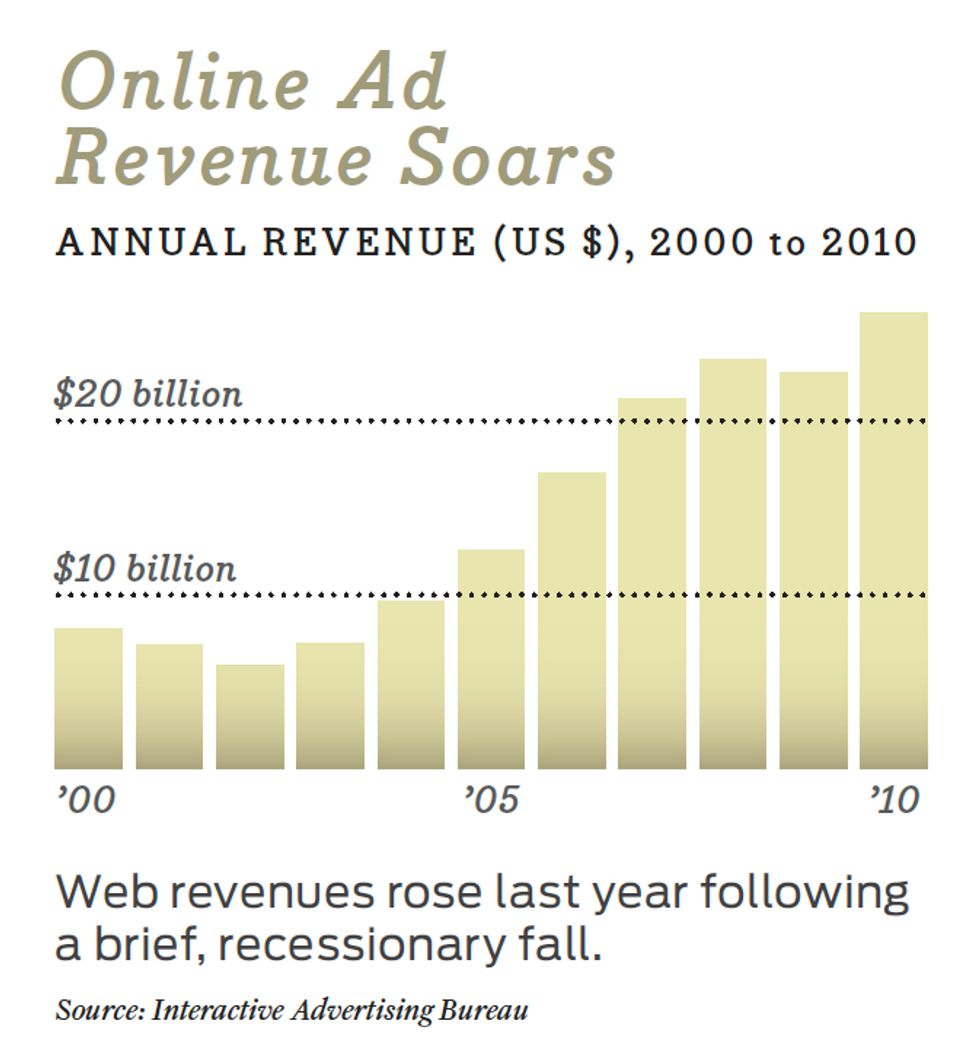

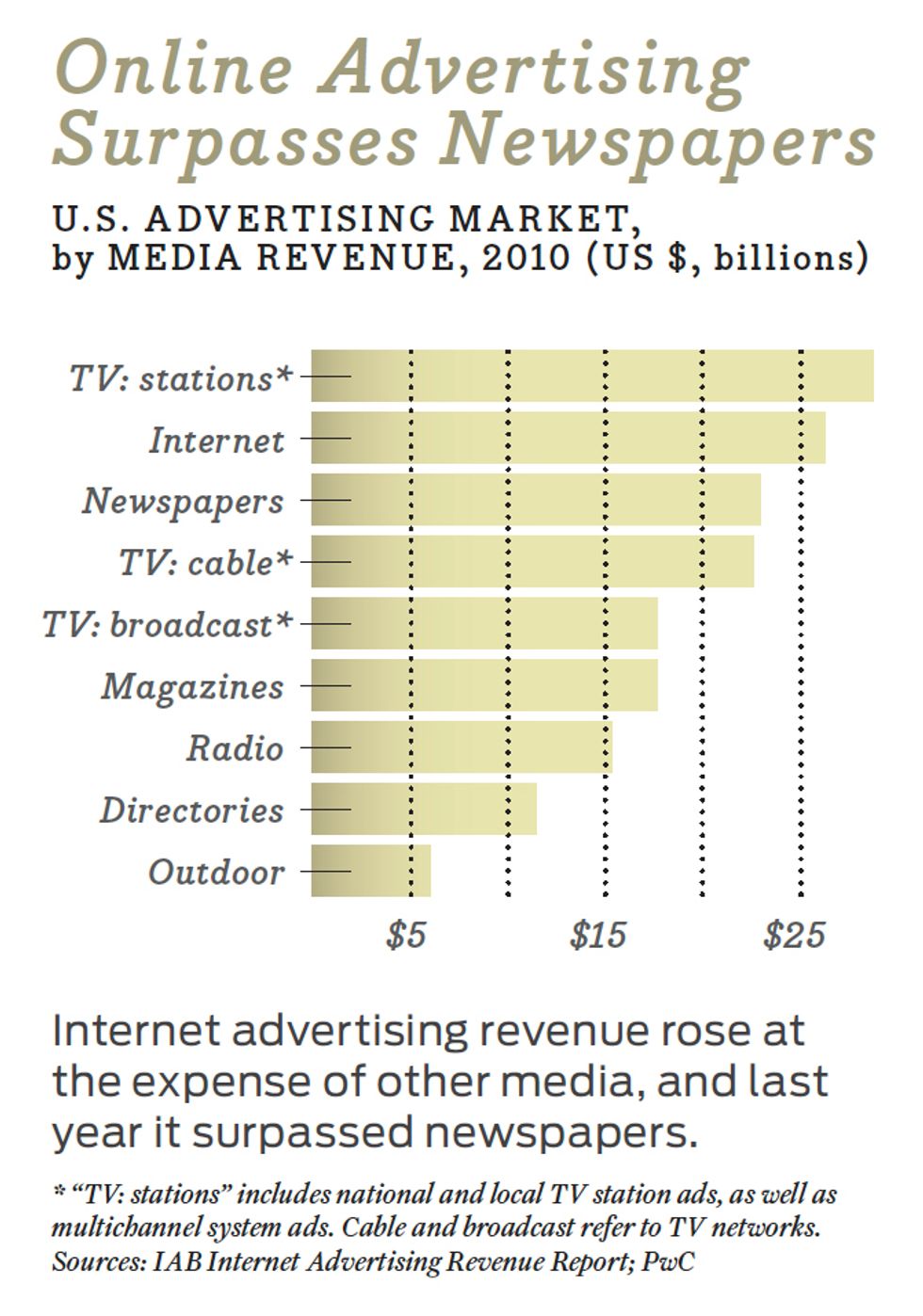

According to the Interactive Advertising Bureau, U.S. advertisers spent $25 billion online in 2010—representing about 15 percent of the $164 billion U.S. ad market and, for the first time, a bit more than their spending on print newspapers. That was no small milestone. But here’s the thing: According to eMarketer, 31 percent of Americans’ media-consuming time in 2010 was spent online. Which means, speaking broadly, marketers valued new-media time only half as much as old-media time. And that’s the rose-colored view. Chris Anderson, curator of the TED Conferences, recently crunched numbers from Nielsen, Forrester Research, the Yankee Group, and other modelers to synthesize the value, medium by medium, of an individual’s time. Globally, print publications fetched $1 per hour of reader attention. TV got a quarter for a viewer hour. Online fetched “less than a dime.”

Why is online advertising such a poor stepchild? Well, extremely delightful and informative books with pale-blue and white covers have been written on this subject, but let’s reduce the problem to its essence: The endless supply of online content means an endless supply of places where ads could go, which by definition depresses demand and, with it, price. Period.

The second problem is more basic still. Ever click on a banner ad? Have you? Ever? Of course not, because why would you leave what you’re doing—especially socializing—to go listen to a sales pitch? The click-through rate, industry-wide, is less than 1 percent—and chalk some of that up to mouse error and click fraud. Some advertisers deal with this problem by popping ads into your face, blaring audio, or subjecting you to “preroll” video messages before the video you actually wish to see. As Anderson sagely observed to a Madison Avenue audience, that was an acceptable quid pro quo in the days of passive TV viewing. Online, though, users are active and in control. “If you take control away from them,” he said, “they will hate you.” Or, put another way: Online, all advertising is spam. These two structural problems leave two possibilities: Either advertising will never be the force in new media that it was in the five predigital centuries (a theory to which I personally subscribe), or someone will crack the code.

The holy grail, if it exists, resides in online advertising’s central advantage: the ability to mine data and target individuals with an offer relevant to their lives and interests. In the case of social networks, there is also the ability to target friends of existing customers—what venture capitalist David Pakman calls “the most powerful form of advertising ever created, not counting search.” Not only is such targeted advertising on average twice as lucrative as conventional ads, it can fetch 100 times as much revenue as mere spam, the sort that pushes random teeth-whitening miracles and predatory-loan-shilling dancing silhouettes. That’s why Pakman believes Facebook’s valuation will rise even higher.

“Social networking is a winner-take-all market,” Pakman says. “They run the table.” His firm recently bankrolled a start-up heavily dependent on Facebook in the social-advertising arena.

On the other hand, that very lucrative targeted messaging has another undesirable effect: It gives us, the target, a condition that experts call the heebie-jeebies. A word about data mining: It is automated and essentially anonymous, but it engenders a creepy sense of privacy invasion and personal violation. Which is why the Federal Trade Commission (FTC) and the U.S. Congress are warning the industry to fix the privacy problem or permit the government to fix it for them. As Anderson sums up the situation: “We’re in danger of becoming stalkers. That strategy is going to end badly.”

Nor is it beginning all that magnificently.

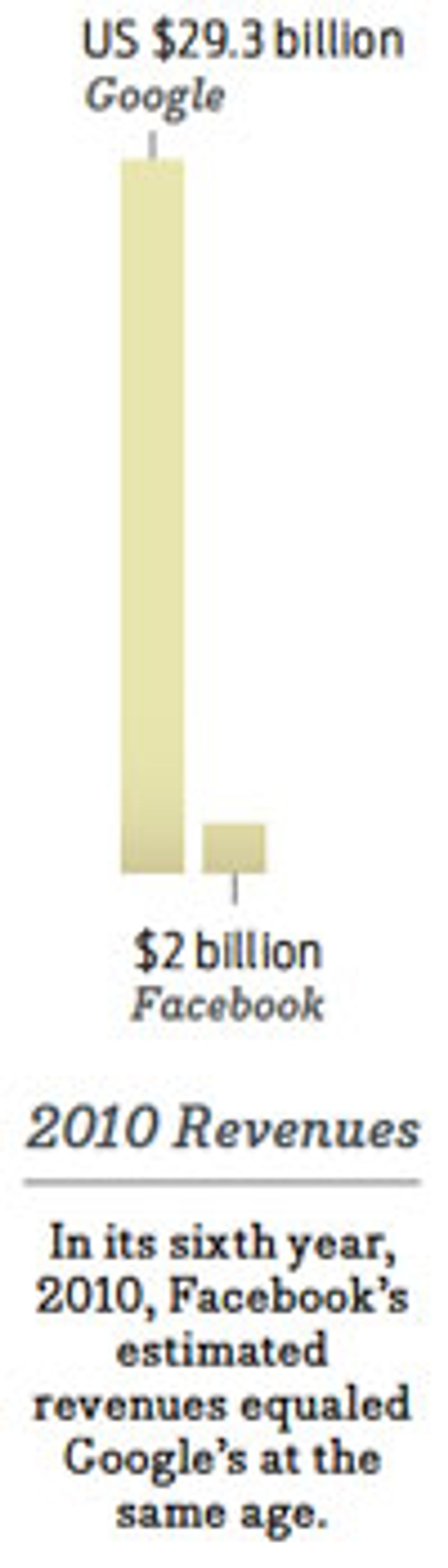

Facebook and Google’s YouTube themselves achieved milestones in 2010. Both are said to have eclipsed $1 billion in ad revenues, and both have reportedly become cash-flow positive. Twitter has only just started attempting to monetize its microblogging utility, but it has similarly altered human behavior on a large scale. Absolutely nobody questions the transformative qualities of these services, nor their extraordinary reach. At this writing, Facebook boasts approximately 600 million users. At current rates of growth, by 2020 its membership will exceed the population of Earth, plus the International Space Station and the planet Krypton. Yet, as Pakman recently estimated, it generates no more than $3 per user per year in revenue (compared to Google, which brings in about $25 per user)—and a huge chunk of the revenue comes from the social-gaming firm Zynga to sell player credits for titles like FarmVille, itself a Facebook app.

Furthermore, Facebook’s priceless asset is not its incomparable reach but its incomparable data set. Should legislators or regulators intervene in the name of privacy—maybe by mandating a simple way for anyone to opt out of tracking—the value and sustainability of Facebook’s data trove would be vastly degraded.

And that’s not the only dark cloud. Facebook’s ad strategy hinges not on ads that appear on Facebook pages but rather those served to third-party sites seeking to benefit from Facebook’s data and reach. This strategy employs Facebook Connect, a bag of tricks that let developers build Web applications that invite visitors to share information with their friends. For instance, such an application allows subscribers to Netflix, the movie-rental service, to tell their friends which movies they’ve seen and how well they liked them.

It is precisely such third-party transactions that the FTC is at the moment proposing to regulate. Furtherfurtherfurthermore, not everyone on Madison Avenue is persuaded that social affinities are such a magical predictor of purchasing behavior. “This is old math,” says Rob Norman, CEO of the media-buying colossus Group M North America. “It’s the Bell Labs’ ‘network neighborhood’ theory of selling long-distance calling plans. ‘Birds of a feather flock together’ blah, blah, blah.” That’s a decent theory but so far, he says, worthy of only “the Scottish Verdict: unproven.”

So hold those thoughts for a moment.

If social targeting indeed represents the second most powerful ad engine in history, the first is surely Google search, which allows advertisers to pursue not those it suspects of being prospects but those raising their hands with search terms hollering “Yoo-hoo! I’m over here! And I’m looking for a deal on a new television.” Google’s 2010 revenues were $29 billion—equivalent to the monthly U.S.–China trade deficit, the Harvard endowment, or the GDP of Latvia plus the market value of the Philadelphia Eagles when Michael Vick is staying in the pocket and refraining from killing dogs. In short, that’s a chunk of change. It is so big, in fact, that nobody much sweats about when or whether YouTube will be significantly profitable, much less about how Google will amortize the $1.65 billion it paid YouTube’s Chad Hurley, Steve Chen, and other owners.

By the same token, as the default platform for video distribution in the Milky Way galaxy, YouTube probably doesn’t care how quickly Anderson fills with blind rage upon being presented a 20-second preroll ad before a 2-minute video of kittens on a sliding board. For those who want free content, says Norman, putting up with commercials “is an occupational hazard,” and necessary, at least up to a point. The balance of ad time versus content time, he believes, must and will find its level. Meanwhile, the display ads on YouTube’s home page have TV-like reach and “are of enormous value to advertisers. I don’t think there is any question about that.”

What YouTube mainly has going for it is its enormous value to users. In addition to being a bottomless bowl of video snacks, it provides convenient and free distribution for the genius and stupidity of countless video civilians. If Google executive chairman Eric Schmidt’s vision is realized, it will also be the central purveyor of all video content, amateur and Hollywood alike, worldwide. For ever and ever. To this end, he has spoken of a 15-year monetization plan including not just advertising but also subscriptions and micropayments. On that journey, he might want to get started right quick.

If YouTube is profitable at $1 billion in revenues, it ain’t by much. Acquisition of Hollywood content means fat licensing fees, and streaming all the world’s video requires vast network capability beginning—but only beginning—with bandwidth. Alas, even in developed countries, the amount of available fiber and wireless bandwidth is insufficient to convey today’s peak loads, much less tomorrow’s. “I was sent on a jaunt for one client to buy as much bandwidth and distributed architecture as I could,” says Tony Greenberg, chief executive of RampRate, the IT infrastructure consultancy. “I had an unlimited budget, but the Internet didn’t have enough capacity.”

Google chews up 10 percent of the Internet’s capacity, and it has recently been speculated that much of that share is in the form of as-yet-unused optical cable, or dark fiber, that’s actually owned by Google. Rather than paying a $500 million annual YouTube bandwidth bill, the company is known to conserve cash by “peering”—trading its excess bandwidth with Internet service providers, like Verizon, for access to their networks. But so what? To Google’s accountants, the barter still represents a gigantic overhead expense.

And it’s not the only one, as Greenberg notes, his voice rising in gathering annoyance. “In the cost of streaming media, I’m sick and tired of everyone talking about x pennies to move a movie on Netflix and then quoting only bandwidth cost. That’s like computing the cost of a bathroom based on the price of toilet paper. You have to deal with the ability to scale, the servers, where the servers live, how it’s routed, what the fault tolerances are in terms of milliseconds. And then there’s 100 engineering and application issues that can go awry.”

That’s why, he says, so many massively multiplayer online games are defunct, and why pioneering social network Friendster, outside of Asia, is more like Dumpster. And why Twitter crashes frequently.

Ah, Twitter. Permit me to dispense with this perfunctorily: It is hard to imagine Twitter prospering long-term as a stand-alone company. Oh, the microblogging utility is surely utilitarian. For those who tweet among themselves, it’s a means to make all life experiences interactive. For those who monitor the Twittersphere, it is a near-perfect, real-time zeitgeist engine. These are revolutionary benefits, but will the revolution be monetized? That entirely depends on the rather dubious value of “promoted tweets.”

“We wanted to do that in a way that was very organic to Twitter and didn’t seem foreign or in any way clash with how people were using the product,” says Twitter cofounder Evan Williams. "Basically, we give companies the ability to give visibility to a topic that they want to give visibility to, and then when people see that and they click on it, they see a tweet from that advertiser. We have a few dozen advertisers who have gotten phenomenal results, and we’re ramping that up now."

Maybe, but here again, a huge obstacle is defeating online inertia.

“If I’m going to be interrupted during a tweet, I want a deal,” says Peter Hirshberg, CEO of the agency Reimagine Group and former chairman of Technorati. But such promotional offers are more or less the antithesis of brand building and therefore not necessarily attractive to leading national advertisers. “The point of a brand is to create brand equity and brand loyalty,” Hirshberg says. The point is definitely not to attract bargain hunters, who are by definition the least loyal, least profitable customers. Many observers therefore assume Twitter will be gobbled up by Google or somebody else—perhaps as a competitive hedge against Groupon, the daily-bargain site, or Foursquare, the location-based social network.

So there. We’ve reduced the battle of social-media titans to Google/YouTube and Facebook. But who prevails? One of them? Both of them? Neither? That answer probably hinges on who dominates in three areas: mobile search (it’s basically the same as search, but on wireless devices, with a few more branches but not really the Foursquare thing), e-mail, and e-currency.

In mobile search, Google doesn’t just dominate—it enjoys a virtual monopoly. It also obviously has a huge advantage in e-mail, with its Gmail service, but Facebook, with its new combined e-mail/text/Facebook-message application, is trying to move into that territory—and thereby start siphoning a huge contextual-advertising revenue stream.

For my money, though, the segment to keep your eye on is “Facebook credits,” the virtual currency now used primarily in places like FarmVille, to buy that game’s own in-house money—say, to purchase a virtual cow. I say it will evolve into the long-sought-after mechanism for online micropayments. And you’re reading it here first—or maybe the second or 18th time, because the thought isn’t unique to me. But the other 17 folks are onto something. As smartphones evolve into transactional tools, Facebook credits could someday function as scrip in the brick-and-mortar world as well. Right now Facebook takes a 30 percent commission; if it can make the system work at 0.3 percent, it will not only overtake the rest of the social media, it will overtake Switzerland.

So, all of the above having been chewed over, the question remains: Who wins? Well, before we get there, I should probably own up to misleading you, because the three queries this essay used as points of departure leave out a possibility, namely that…

4. Those three questions are irrelevant! What if we evolve from an Internet-cloud environment to an app environment—in which case Steve Jobs, who defined his business in 1984 by portraying the competition as Big Brother, could wind up as Big Brother himself? As app-centric mobiles and tablets increasingly dominate our online lives, perhaps the CatRattle app or something else will materialize to make us all forget that Mark Zuckerberg, Chad Hurley, and Evan Williams ever existed.

Maybe yes, maybe no; my forecast is cloudy with a strong chance of iPads. But I must delay no longer. The assignment here was to make a prediction, and with all the above-mentioned caveats, and the further disclaimer that this is but one man’s opinion, I will boldly do just that. The dominant online force with a significant social-media component over the next 20 years will be:

Amazon.com.

This is part of IEEE Spectrum’s special report on the battle for the future of the social Web.

About the Author

Bob Garfield, cohost of WNYC’s “On the Media,” distributed by NPR, and longtime Advertising Age columnist, is author of The Chaos Scenario, which describes the collapse of mass media and mass marketing as a by-product of the digital revolution. He says that when he first floated his theories in 2005, he was wisely dismissed as a hysterical crackpot, whereas now, a mere six years later, he is widely dismissed for belaboring the obvious. He gives a précis of those theories in “The Revolution Will Not Be Monetized.”