This is a guest post. The views expressed here are solely those of the author and do not represent positions of IEEE Spectrum or the IEEE.

A couple of years ago, I raised eyebrows when I argued that autonomous vehicles would be a trillion-dollar industry. It turns out that I was being too conservative: A recent report by Intel and Strategy Analytics estimates that autonomous driving technology will enable markets worth upwards of $7 trillion. This number includes new kinds of mobility services and applications that, according to the study, will be made possible by advances in sensing, vision, simulation, mapping, vehicle-to-vehicle communications, and other areas.

But here's the thing: Many of the tech companies, big and small, working on advanced vehicle technology seem focused on one thing: eliminating the steering wheel. In other words, these companies are targeting fully autonomous driving, or what is known as Level 4 and Level 5 autonomy, and by doing so, I believe they're ignoring a sizeable chunk of that multi-trillion-dollar opportunity: The hundreds of millions of conventional cars that will roll off assembly lines and could benefit from automated driving features. So what we need is more startups to build the systems that, while they won't allow for complete vehicle autonomy, will help people drive less and drive more comfortably.

Over the past several years, many observers have envisioned a future of car ownership becoming a thing of the past. It now appears certain that ride sharing, electric powertrains, and autonomous features will reduce the cost of getting from point A to point B: miles will get cheaper. Historically, lowering the cost of most products has led to more consumption: refrigerators in garages, televisions in every room, computers on our desks, pockets, and wrists. I believe it will be the same for miles: A growing affluent global population will command many more miles, and many more vehicles. Over time, an increasing portion of these vehicles will not be equipped with steering wheels. But it will take quite a while. Starting from zero today, they will number in the dozens in the next half-decade, and then millions in the next few decades. In the meantime, I expect conventional vehicle sales to continue growing until at least the second half of the century.

All of which is to say there is a big opportunity today in putting automated driving into regular cars. Nearly 95 million human-piloted vehicles were produced in 2016. Assuming hundreds of millions of cars and a few thousand dollars of value in the sensors, software, and services going into each vehicle over the next decade, then we're back in the trillions of dollars. To capture that market, companies need to envision how automated driving will be defined and offered to consumers.

My guess? Not very differently from how it is being marketed today. Power steering doesn't mean not steering (though it did allow for holding a cup of coffee while piloting a car), and adaptive cruise control doesn't mean sitting cross-legged (even though it lets you rest your feet). Furthermore, braking isn't entirely left up to cars with automatic emergency braking. My expectation is that “automated driving" will continue to be positioned as “driver assistance." Early versions of driver-assistance systems, with limited capability, will require drivers to be always ready to take over, as with Tesla's Autopilot. More advanced, expensive versions will offer more autonomy, requiring drivers to respond in a few seconds if there's an emergency. But I believe that even with the most advanced versions, drivers will have to agree they are responsible for the safety of all the passengers in the vehicle, and must be alert at all times.

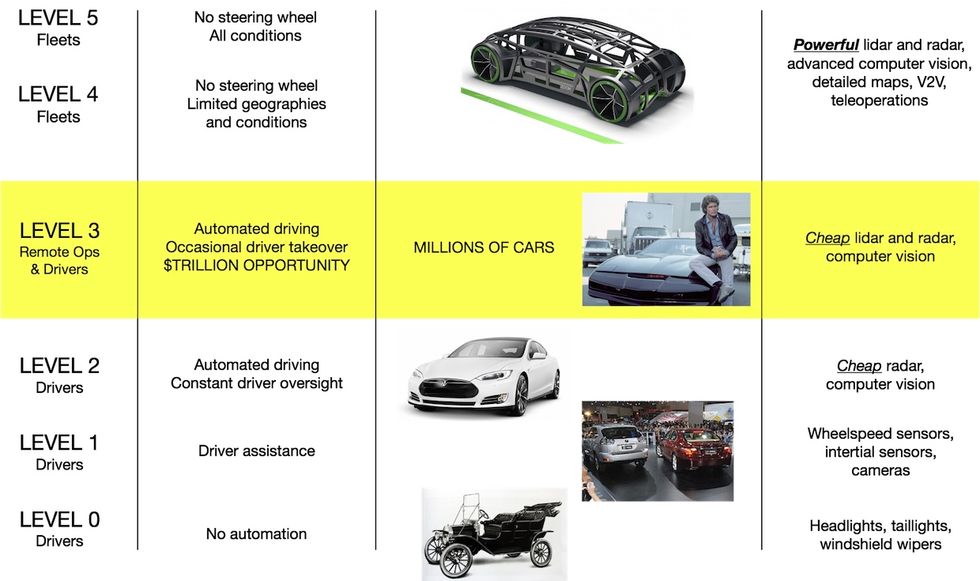

Traditional automotive suppliers like Bosch, Delphi, Denso, and Continental have historically done a good job providing technologies to assist drivers (Level 0 to 2). As we move to Level 3 and above, there will be a need for cheaper sensors, as well as new kinds of services for vehicle supervision. One example would be a tele-operations service that charges for overseeing and being responsible for a vehicle when it operates autonomously. In the case of robo-taxis, they would be owned by a service that manages and tele-operates fleets of such vehicles. Level 3 cars, being consumer products, will be very sensitive to the cost of the sensors and how easily they can be integrated into assembly lines. Level 4 and Level 5 vehicles, which will likely be owned by fleets, will not be as sensitive to cost, but will require far greater performance and reliability. By going straight for Level 4 and 5, most of today's driverless tech startups are skipping past a massive opportunity in Level 3.Image: Lux Capital

Traditional automotive suppliers like Bosch, Delphi, Denso, and Continental have historically done a good job providing technologies to assist drivers (Level 0 to 2). As we move to Level 3 and above, there will be a need for cheaper sensors, as well as new kinds of services for vehicle supervision. One example would be a tele-operations service that charges for overseeing and being responsible for a vehicle when it operates autonomously. In the case of robo-taxis, they would be owned by a service that manages and tele-operates fleets of such vehicles. Level 3 cars, being consumer products, will be very sensitive to the cost of the sensors and how easily they can be integrated into assembly lines. Level 4 and Level 5 vehicles, which will likely be owned by fleets, will not be as sensitive to cost, but will require far greater performance and reliability. By going straight for Level 4 and 5, most of today's driverless tech startups are skipping past a massive opportunity in Level 3.Image: Lux Capital

Based on that scenario, it's possible that, in the future, car owners would be able to purchase a kind of tele-operations plan. This plan would have their vehicles remotely supervised by human operators while in automated driving mode. That would mean that, for a price, the liability is handed off from the driver to the operator. This kind of monitoring service might still require the driver to be sitting in the driver's seat and be ready to take over if necessary, but it would have the remote operator overseeing pretty much all of the vehicle's functions as it drives itself.

Another possible scenario, when we start approaching Level 5, is that regulations will mandate a certain degree of oversight and central control of the vehicle if passengers want to be “licensed" to divert their attention elsewhere while sitting behind the wheel. Cameras and eye-tracking technology can easily determine if a driver is alert, so we can imagine a situation where a driver who is not licensed to divert his or her attention get distracted, and sirens go off inside the car to prompt the individual to regain focus.

In addition to tele-operation services and passenger-monitoring technologies, another promising area for driverless tech startups are more affordable vehicle sensors, including radar, lidar, and other ways of scanning a vehicle's surroundings. These technologies will certainly be key to bring automated driving to hundreds of millions of conventional cars.

For example, Luminar, based in Palo Alto, Calif., and Orlando, Fla., and several other startups, are building affordable replacements for rotating lidars—the big spinning cylinders you see on the roof of many self-driving vehicles. These are made by Velodyne, which pioneered and has since dominated the 360-degree lidar space. Indeed, Velodyne does have a low-cost version in the works, based on solid-state technology, as does Quanergy, a startup based in Sunnyvale, Calif. The mechanical versions offer a large field of view and a high degree of resolution and precision. It remains to be seen as to whether the solid-state alternatives can even be good—and cheap—enough for Level 3 or 4, but recent demonstrations show promising steps in that direction.

Not everyone is convinced that lidar is necessary, though. Elon Musk has gone as far as to predict that radar can obviate the need for lidar altogether for driver assistance. Current Tesla models have no lidar units, and it doesn't seem like the company has plans to add any in the future. We know that Tesla's Autopilot (Level 2) works reasonably well, and Autopilot-related accidents appear to have mostly been the result of drivers abusing the technology.

But I remain firmly in the pro-lidar camp. I think it is inevitable that Level 5 robocars will use many advanced Luminar-style lidar units, and I expect that going to Level 3 and 4 will require some basic form of lidar as well. These units will cost a few hundred dollars or less, and perhaps be coupled with cameras and radar, to better navigate the car through the inevitable corner cases.

At my firm, Lux Capital, we funded Silicon Valley startup Zoox to reinvent the car and revolutionize surface transport by operating a fleet of robo-taxis for consumers. We have also funded Aeva, a stealth startup that is developing new sensing technologies to address the yet-to-be-solved challenges required for Level 3 through Level 5 automation. These challenges include lidar's limited range, radar's low resolution, and inertial sensors that cost too much. Aeva's current system fits nicely into existing automotive design and assembly, which in this industry is as important as low cost.

So will we have fully autonomous cars in the future? Yes. But until then, I expect everyone to enjoy the benefits of automated driving technology in the comfort of their own vehicles. I hope the tech industry and VC firms will focus less on the holy grail of cars with no steering wheels and more on enabling millions and millions of regular cars to drive more autonomously, reliably, and safely in the near future. Attention entrepreneurs: Don't pass up this trillion-dollar opportunity!